Hi, I’m a personal finance expert who loves to help you out! I’ll answer your question within a business day. Pinky swear.

In recent years, micro-lenders have cropped that let you get a quick loan to bridge the gap to payday, or buy a big-ticket item that you (apparently) desperately need. Pay on demand apps fall into the same category, with a twist: you’re accessing your wage early, rather than getting an expensive loan. Does that mean pay on demand apps are a good deal?

Maybe, and maybe not, depending on how often you need to use them. Pay on demand services cost money every time – usually around 5% of the amount you’re borrowing – which can add up if you need to use it a lot. But, they can also be a lifesaver if you’re in a pinch, and they’re a safer option than other forms of micro loans.

Here, we’ll look at:

How do pay on demand apps work?

Pay on demand apps are sometimes called wage advance apps, because they let you access a portion of your pay before you’re due to get it. To sign up for the service, you’ll usually have to download the app, fill in some personal details about yourself, your employment and your wage, and connect to your bank account. The app can calculate how much you can withdraw that day based on your pay cycle.

Later, when your wage is paid into your bank account, the app deducts your amount owing automatically as either a lump sum, or across a few pay cycles.

It’s actually a pretty neat little system, providing you can use it wisely and only when you really need it.

There are some limitations on what you can access; for example, you might have to withdraw at least $50, and not more than a quarter of your wage. You’ll have to compare providers to see what they allow.

Of course, it’s not a free service. Each time you use the app, you’ll be charged a fee. The fee might be a percentage, or it might be a small flat fee.

What types of pay on demand apps are there?

There are three types of pay on demand services:

Pay on demand apps: these are dedicated apps you download to access a portion of your pay early, for example Beforepay and MyPayNow.

Banks: some banks offer pay on demand if you have an account with them. For example, Commbank offers an AdvancePay feature that works in much the same way as pay on demand apps.

Your employer: some employers offer pay on demand as a company perk. Your employer essentially partners with a pay on demand platform and lets you access your pay early through its software.

What pay on demand apps can you get in Australia?

There’s a few types of pay on demand offers to compare:

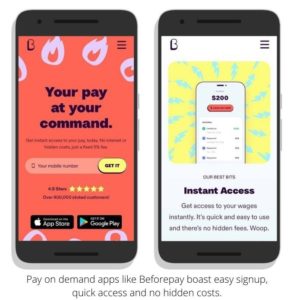

Beforepay

No Interest or Hidden Fees

With Beforepay you can access up to $2,000 of your pay for a 5% fixed fee. To decide your limit, Beforepay will securely connect with your bank to see your salary details.

- CommBank AdvancePay. If your wage is paid into a CommBank account, you might be eligible to use their AdvancePay feature. Fees start at $5, and you can request to borrow between $300 and $5,000.

- MyPayNow. You can advance up to a quarter of your wage with MyPayNow for a 5% fee.

- Earnd. Your employer can sign up with the Earnd platform to let any employee access a portion of their pay early.

How much will you be charged?

Costs vary between platforms, but you’ll generally be charged either:

- A percentage of the amount you borrow (5% seems to be the standard rate)

- A flat fee on a sliding scale, depending on the amount you withdraw

You might also be charged late fees if you can’t repay the amount on time, although some services like Beforepay don’t charge any default fees. You’ll need to make sure any of your other regular direct debit commitments (like streaming services or phone payments) don’t leave your account empty when your repayment comes a-knocking.

Some late fees can be as hefty as an interest rate; for instance, CommBank’s AdvancePay charges 14.90% on money you owe.

Are pay on demand apps safe?

If we’re talking safe from fraud, then generally yes, pay on demand apps seem to be equipped with security and privacy safeguards, including encryption of your data and secure access to your bank account.

However, since the fresh face of pay-on-demand is so new, they’re also a little unregulated; for instance, they’re not required to do the same pre-approval checks that banks and lenders are when giving out loans or credit cards.

That means no one is really checking to make sure you can repay the money you’ve borrowed. So, if we’re asking if pay on demand is safe for you personally, that will depend on how frequently you need it, and whether it’s getting you into debt.

| If you find yourself in debt to pay by demand: There are ways you can get on top of your debt, like using a balance transfer credit card. Balance transfers let you move debt onto a credit card and pay 0% interest for a period, allowing you to pay it down without extra fees slowing you down.Unfortunately, there’s no way to transfer your pay on demand debt directly to a balance transfer, so you’d need to work around it by: • Paying your debt with a credit card • Transferring the credit card debt to a 0% balance transfer offer credit cardBeing approved for two credit cards will depend on your financial circumstances, so make sure you check the PDS of each card and are confident in your plan before you apply.Here’s a simple guide to paying off debt with a 0% balance transfer offer. |

Pay on demand apps vs Payday loans

They might share some words and similarities, but these two types of loan shouldn’t be confused.

Pay on demand apps let you some of your wage before payday and charge a small fee for each transaction. The money is repaid over a series of weeks each payday.

Payday loans operate in much the same way in that you can request a small-ish loan (up to $2,000 generally, but some allow more), which is repaid when your wage is deposited into your account. The repayment timeframe can be as short as a few days or up to a year.

The key difference is that payday loans are the used-car salesmen of loans: they’re notorious for their exorbitant ongoing fees and surprise charges. And, since they allow you to borrow more than pay on demand apps (which are usually capped at a percentage of your wage), it can be harder to get on top of the repayments once you slip behind.

Payday loans also tend to be less forgiving, charging dishonour fees of around $79 and higher.

To show you the difference between three types of loans, let’s compare a pay on demand loan, a payday loan and a 0% interest credit card on a $500 loan.

| Service | Transaction fee | Total transaction fee | Ongoing fee | Total cost (2 month payment) |

|---|---|---|---|---|

| Pay on demand loan | 5% of loan amount | $25 | None | $25 |

| Payday loan | 20% of loan amount | $100 | $20 per month (4% of amount borrowed | $140 |

| 0% interest credit card | None | $0 | $10 per month (waived if card not used) | $20* |

*It’s important to remember that a monthly credit card fee is only charged once, whereas you’ll be charged for every loan transaction using pay on demand or payday loans.

Payday loans have come under fire for targeting desperate Aussies, and should probably be seen as a last resort. Have a think about a 0% interest credit card, or a no annual fee credit card instead of a payday loan.

Will it affect your credit score?

Beforepay and MyPayNow states that applying and defaulting on repayments won’t affect your credit score. CommBank reserves the right to report AdvanceNow unpaid repayments to credit bureaus, which mayaffect your credit score.

Having said that, pay on demand won’t help you get a better credit score either, so you’ll need to decide if that’s important to you. Small transactions on a low-cost credit card can offer similar services to pay by demand and boost your credit score at the same time.

Will your employer know if you access your pay early?

Pay on demand is between you, the app and your bank account. Even if your employer uses a platform like Earnd to offer pay on demand, they won’t know who uses it.

Are you eligible for pay on demand?

There are generally fewer pre-approval checks for pay on demand, and softer eligibility criteria. To set up a pay on demand account, you’ll probably need to:

- Receive a regular salary into your bank account

- Have regular, ongoing employment

- Earn the minimum set by the app (usually around $300 per week)

- Pass the app’s credit assessment, which usually involves checking your income and spending through your bank account

Benefits and drawbacks of pay on demand apps

Pros

- Easy, quick access to money when you need it

- May be no credit checks involved

- Usually cheaper than payday loans

- Managed from your smartphone

- Generally low fees per transaction

Cons

- Fees can add up if you miss payments

- Minimum loan amounts can be as high as $300

- Missed repayments can snowball

- Not building a credit score

- Unregulated market for now

Alternatives to pay on demand

If you’re thinking about pay on demand because you’re consistently living on the financial edge, you might want to consider some other options.

- Put a budget in place: the only way to pay down debt and stay out of it is to spend less than you earn. Make a basic budget to repay your outstanding money, cut down on expenses and ask for financial assistance from big companies you owe money to.

- Use a credit card instead: credit cards may help you save money on fees and earn rewards, cashback or perks that cut your living costs.

Using credit cards as an alternative

Did you know lots of credit cards have flexible repayment options that rival – and sometimes outdo – pay on demand services? In fact, they can be a better deal than Buy now pay later as well. With some credit cards, you can split your repayments into smaller, interest-free chunks and pay it off over several months, rather than just four weeks.

Here’s how you can use a credit card to Buy now pay later, and see if it works as a better option for you than pay on demand apps.

Another perk from credit cards are the extras you get for free. Many cards give you:

- Free travel insurance

- Discounts with partnering businesses like Spotify and DoorDash

- Reward points when you spend, that you can redeem for free stuff

- Purchase protection, so you get the best price

- Big rewards points bonuses when you sign up

If you’re able to pay back your borrowed amount each month, or set up a flexible repayment option, you won’t have to pay interest on your credit card. You’d have to weigh up if the perks made any annual fees worthwhile, which would depend on how you live (for instance, if you travel, the bonus points and free travel insurance might already save you more than you’ll spend on the annual fee).

Compare your fees with pay on demand to the ongoing expenses of the card, and see which one works out better for you.

Comparable low interest rate credit cards:

- Great Southern Bank Low Rate Credit Card: no annual fee the first year, $49 after that, plus a low interest rate.

- Bankwest Breeze Classic Credit Card: $49 annual fee, and 0% interest for 24 months.

0% interest rate credit cards:

No annual fee credit cards:

Low-cost rewards cards:

Verdict: Should you use pay on demand apps?

If you really do need your pay early, pay on demand apps can be helpful. They’re easy to use, quick to apply for, and pride themselves on taking 60 seconds to have the money in your account (or, up to one business day, in the small print).

They’re a better alternative to payday loans that charge exorbitant fees and ongoing charges.

However, you’ll need to think carefully about how often you need to access your pay early, and whether you’re able to make the repayments. While the fees are small, they can add up if you’re requesting money regularly, and snowballing repayments can get out of hand.

Make sure you weigh up pay by demand apps with other forms of low-cost borrowing, like no annual fee and 0% interest credit cards, that could reward you for your spending in more ways than one.

All rates, fees and offers correct at the time of publication. Please check the most up-to-date PDS and TMD of the credit card or product to make sure it suits you.

Pauline Hatch

Pauline is a personal finance expert at CreditCard.com.au, with 9 years in money, budgeting and property reporting under her belt. Pauline is passionate about seeing Aussies win by making their money – and their credit cards – work smarter, harder and bigger.

You might be interested in

Recently Asked Questions

Something you need to know about this card? Ask our credit card expert a question.

Ask a questionHi, I’m a personal finance expert who loves to help you out! I’ll answer your question within a business day. Pinky swear.

(showing the latest 10 Q&As)

Featured Balance Transfer Credit Cards

NAB Low Rate Credit Card – Balance Transfer Offer

0% on balance transfers for 24 months

Featured Rewards Credit Cards

Apply by 18 Mar 25

{kind=link}